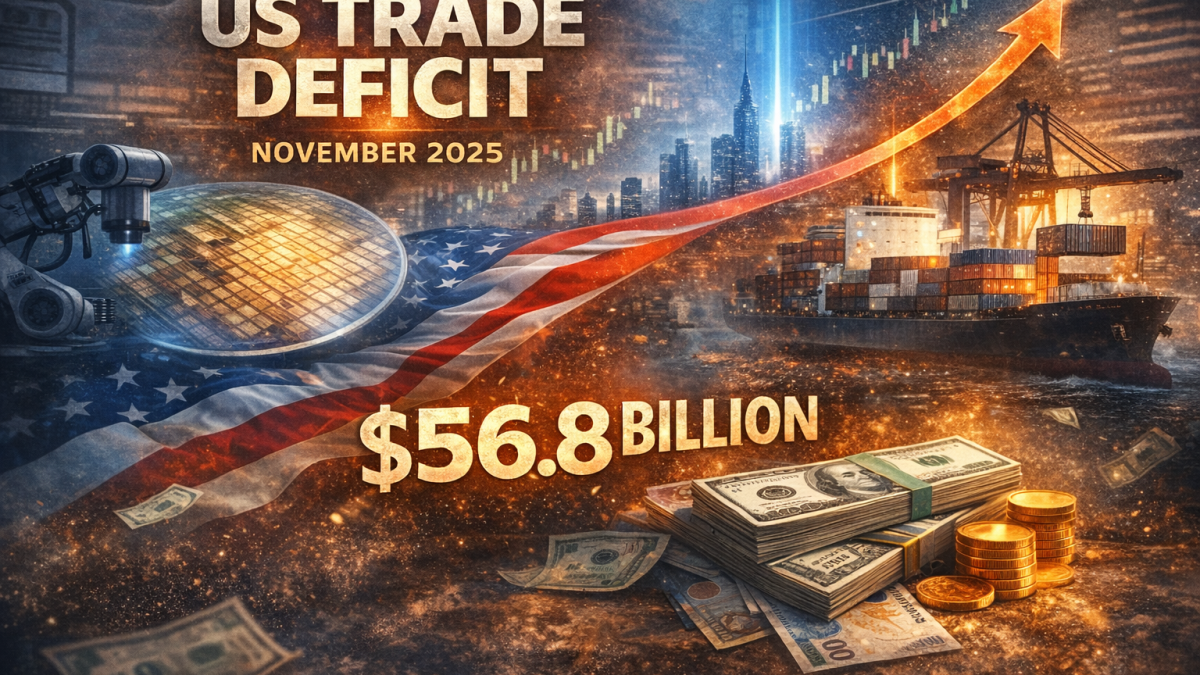

The US trade deficit ballooned to $56.8 billion in November 2025, crushing economists’ forecasts of $43.4 billion and nearly doubling from October’s revised $29.2 billion.

The magnitude of the surge in trade deficit signals intensifying import pressure as American consumers and businesses continue shopping abroad.

The shortfall marks the return of a structurally wider deficit after October’s anomalously narrow position.

It raises fresh questions about whether tariff-related front-loading is masking deeper import momentum heading into 2026.

Breaking down November’s trade collapse

Exports fell $10.9 billion in November to $292.1 billion, down 3.6% month-on-month. Imports jumped $16.8 billion to $348.9 billion, an increase of 5%.

The goods deficit widened dramatically to $86.9 billion, up $27.9 billion from October. Services trade provided a limited offset, with the surplus ticking up just $0.3 billion to $30.1 billion.

The composition matters. Consumer goods and industrial inputs surged into ports during November, a pattern consistent with pre-tariff stockpiling and elevated holiday shopping demand.

Goods imports increased by 6.5% in nominal terms.

Meanwhile, American exports of manufactured goods and raw materials weakened, suggesting that demand outside the US continues to cool.

The damage compounds when we look at numbers from the year-to-date level.

Through November, the goods and services deficit is up $32.9 billion or 4.1% compared to the same eleven-month period in 2024, with imports rising 5.8 percent while exports grew just 6.3 percent.

The deficit with the European Union alone jumped $8.2 billion to $14.5 billion in November.

Dollar and growth implications

The widening deficit lands as policymakers remain watchful about the tension between strong consumption and trade arithmetic.

A persistent trade deficit subtracts from GDP in national accounts, specifically, the calculation measures net exports.

If imports dwarf exports, it can overall growth, though a strong consumer offsetting this through spending growth and inventory accumulation can obscure the effect.

On the currency front, the relationship seems more complicated.

On January 29, as the trade data crossed the wires, the dollar rebounded following Federal Reserve Chair Jerome Powell’s hawkish tone at his press conference on January 28.

Treasury yields stayed flat with the 10-year hovering around 4.26%, as markets digested the Fed’s hold and signals of patience on rate cuts.

Economists and strategists now face a critical question heading into February: whether November’s import surge reflects temporary front-loading ahead of tariff implementation or a structural shift in consumer demand toward foreign goods.

If the latter persists, the deficit could remain above the $50 billion monthly run rate, weighing on first-quarter growth and potentially complicating the Fed’s policy path should import-driven inflation resurface.

Next month’s December trade report, due February 19, will be closely watched.

The post US trade deficit widens to $56.8 billion, far exceeding $43.4B forecast appeared first on Invezz